By Aimee Raleigh, Principal at Atlas Venture, as part of the From The Trenches feature of LifeSciVC

“Travel makes one modest. You see what a tiny place you occupy in the world.” — Gustave Flaubert

Life sciences in April 2026 has, against all odds, been buoyant. The XBI is trading near its 52-week high, we just saw the largest biotech IPO on record, and private financings are continuing apace (albeit with a tilt toward clinical-stage and “de-risked” programs). But even in its periods of resilient growth, the life sciences VC sector is dwarfed by broader tech trends, which are increasingly dominated by AI themes.

We forget sometimes, being embedded in the biotech ecosystem, that the share of venture flowing into life sciences is a fraction of that in the broader market. LifeSciVC highlighted this a decade ago; despite a bull market in biotech back in 2015, our sector was a shrinking sliver of the venture ecosystem. Today, like then, ask 100 people on the street what they picture when they hear “VC” or “startup,” and most will describe a tech company – and today, almost certainly an AI company – not an innovative biotech. As an industry, we are intellectually aware that life sciences is a small piece of the venture pie, but nothing has sharpened that perspective quite like the rise of AI/ML.

For this post, I thought it would be interesting to revisit key statistics across the tech and life sciences investing ecosystems over the last few years, as AI/ML companies have accumulated an extraordinary allocation of mindshare and funding. It’s very likely that tech is in – or soon to be in – an AI-themed bubble. There are lessons to be learned from this cycle, and AI serves as an instructive case study in what happens when a transformative technology wave meets unbounded investor FOMO.

Tech, and increasingly AI/ML companies, command an extraordinary share of total financings

There is no doubt that we are in a transformational moment for AI/ML technology. To quote Sam Altman, “In a decade, perhaps everyone on earth will be capable of accomplishing more than the most impactful person can today.“ But with every cycle of technology advance, there are winners and losers. This cycle won’t be any different, other than the winners will likely be bigger than ever before, and more capital will be deployed into the losers than ever has been previously invested in an emerging venture theme. It’s instructive to evaluate this particular AI/ML cycle, and its differences from (and lessons for) the life sciences venture ecosystem.

I will evaluate the rise of AI/ML investments, and the comparison to the life sciences investment landscape, over the past few years from 2022 on. 2022 marks the beginning of an inflection in tech – or perhaps the start of the exponential portion of the growth curve – and specifically the launch of the current AI super-cycle. While AI investments were certainly made prior to 2022, generative AI began hitting its stride early that year and was increasingly adopted by large enterprises. Early fortunes have been made on the founder, employee, and investor side (SF mansion shortage, anyone?!), but we are still very much in the early innings of the AI/ML capital returns story.

Like any bubble, however, concentration in one area risks over-exposure. While super-cycles come and go, the AI momentum feels different in that orders of magnitude more capital are being deployed than in prior waves. OpenAI is projected to spend ~$30B this year alone on model training costs, with compute costs potentially reaching ~$120B by the late 2020s (source). Moderation is a word rarely applied to investing of any flavor, but we have never lived in a time when the cost of immoderation is so high. Winners will certainly emerge from the AI boom – I suspect, as is typical with platform shifts, there will be a relatively small handful of durable winners and many hundreds of failures.

PitchBook and NVCA’s Q4 2025 Venture Monitor (link) offers a striking view of this concentration. Broadly speaking, “tech” (which includes AI/ML, but also enterprise, consumer, fintech, cybersecurity, crypto, and deep tech) has historically commanded most VC dollars. But 2025 marked an unprecedented concentration within a single category: AI/ML companies captured 65% of total U.S. VC investment – $220B out of $340B – up from 31% in 2022 and just 10% a decade ago (Fig. 1). Life sciences deal value, on the other hand, has remained relatively consistent in absolute terms (10-20%), though it has shrunk as a percentage of the overall pie in recent years given the much larger denominator. If anything, the stability of life sciences financing in the face of this AI supernova is a testament to the resilience of the sector.

Is the exponential increase in financing for AI/ML companies inherently negative for biotech? Not necessarily. This skew likely reflects an expansion of the total venture “pie,” paired with increasing deployment of tech VC dollars toward AI/ML – rather than VCs who invest in both life sciences and tech redirecting life sciences-earmarked capital toward AI/ML.

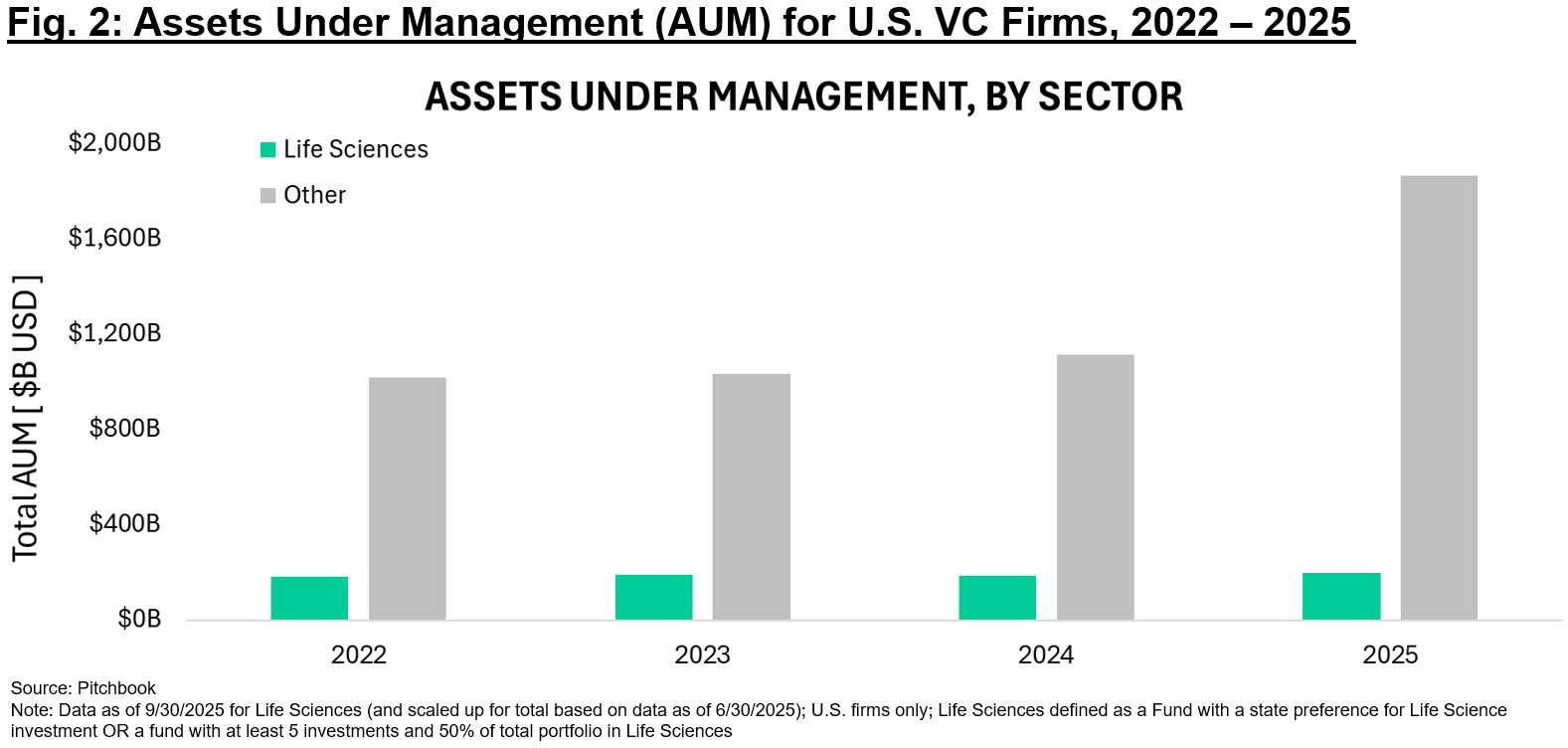

This expansion of total VC dollars deployed is evident in Fig. 2, which illustrates that assets under management (AUM – both deployed capital and dry powder) for life sciences have remained relatively flat at ~$200B year-over-year. Non-life sciences VCs (the majority of which we can assume are tech-focused) have seen AUM grow at a ~20% CAGR from 2022–2025. While we don’t have a precise breakdown, this AUM surge is likely driven by fundraising by GPs (and corresponding LP investment) targeted at AI/ML opportunities.

Thoughts on mass balance — where do all these companies go?

The lifecycle of a typical venture-backed company involves a tenure as a private company, a potential “exit” when it goes public or is acquired, and/or a departure from the VC-backed pool because the company has shut down (technology or program(s) didn’t work, capital ran out, or otherwise). Tracking this flow with a mass balance lens is instructive, and I attempt to illustrate some of these variables below using data from PitchBook and other sources.

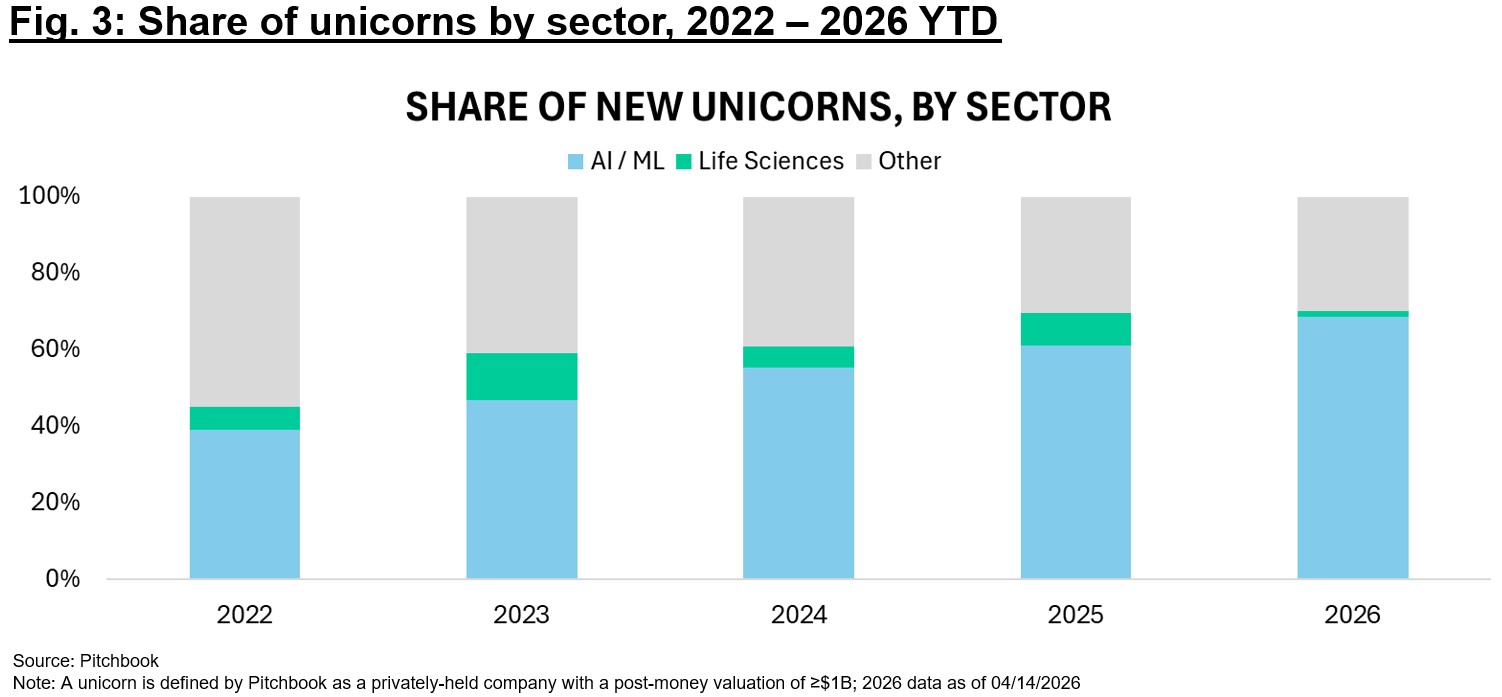

On the private company side, we frequently hear about companies staying private for longer. “Unicorns” – private companies with valuations exceeding $1B – are increasingly common relative to a decade ago, in part because companies have found ways to access large sums of private capital without subjecting themselves to the scrutiny of public markets. The unicorn phenomenon is especially amplified in AI/ML (Fig. 3): over 60% of new unicorns in 2025 were AI/ML companies, and in 2026 that figure is already approaching 70%. Life sciences unicorn creation has been steadier and less common – biotech companies, which need continuous capital infusion to fund clinical programs, generally have more incentive and greater ability to access public markets sooner.

Unicorns in themselves aren’t a bad thing, but with so many companies requiring large sums of financing, it raises important questions about the distribution of returns. Bill Gurley noted in a recent interview that a class of perhaps ~1,000 pre-LLM “zombie unicorns” – companies that raised hundreds of millions chasing the prior wave of tech optimization – sit on GP and LP books at values likely well above their true worth, with aggregate paper value potentially exceeding $1T. This illustrates the risk of the power law of returns: yes, there will be winners, but there will be many more losers. And we are currently financing losers at the highest rate we ever have. Capital is not endless, and not all firms will participate equally in the returns of any given asset class.

Where do these unicorns go when they can no longer sustain high burn rates as private companies? As of 2026, there are roughly 900 active unicorns globally, holding over $4T in aggregate valuation – of which fewer than 5% are in life sciences. A majority will likely shut down over the next 5 years, some will be acquired, and a portion will make it to IPO on favorable terms. The question is how many of these aggregate valuations reflect genuine enterprise value versus inflated late-stage paper.

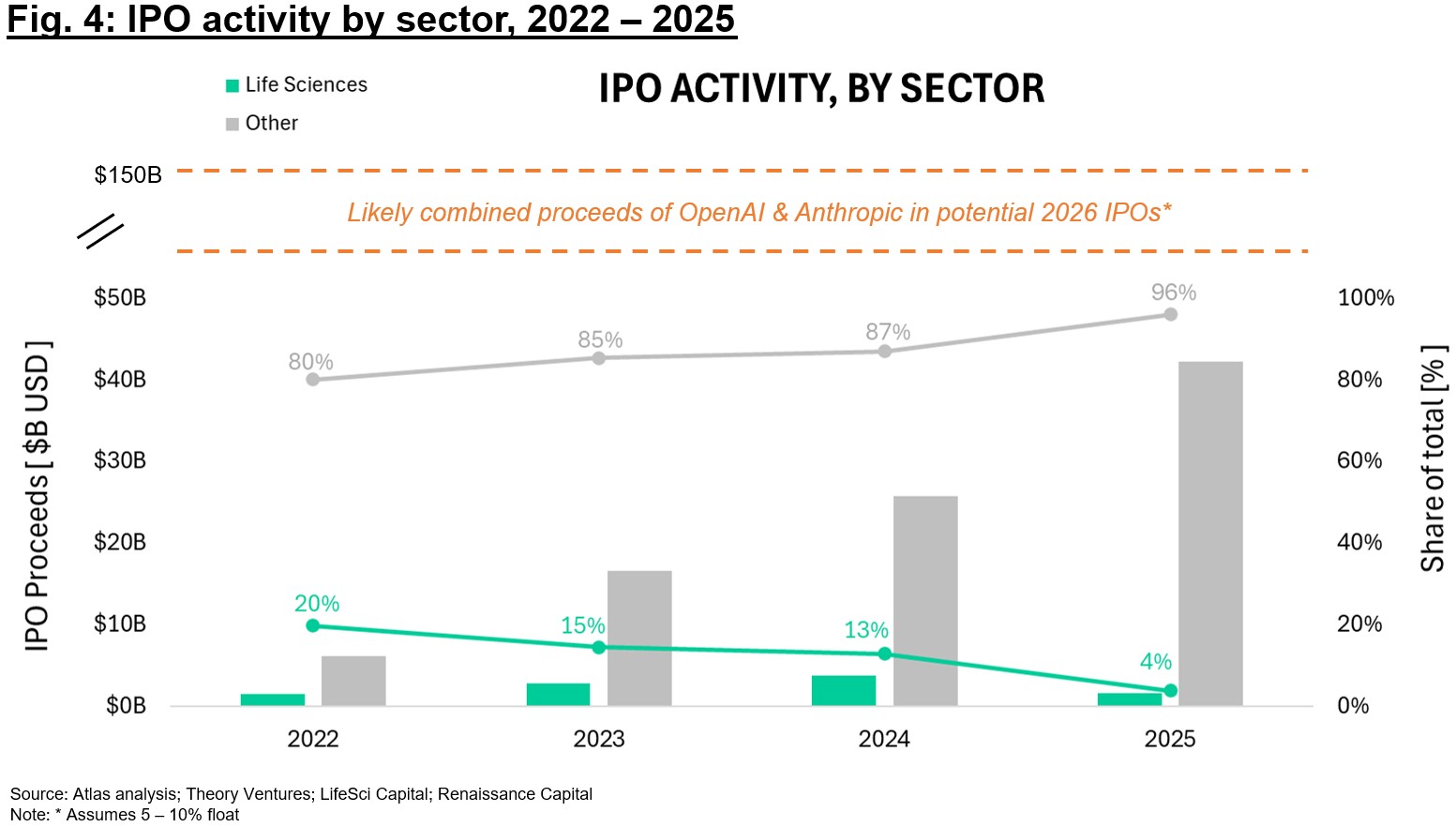

Let’s look at IPOs specifically as a potential “exit” path. Biotech has historically commanded a reasonable share of total IPO volume and proceeds, but the gap has been growing in recent years (Fig. 4). In 2025, biotech represented just 4% of total IPO proceeds – a figure that has been decreasing since 2022. While other sectors (including tech) have recently commanded the lion’s share of IPO volume and proceeds, that divide is about to grow even larger with the maturation and public entrance of AI/ML companies. The potential 2026-2027 IPOs of OpenAI and Anthropic (which would likely each need to raise >$40-100B in an IPO) would individually dwarf the cumulative IPO proceeds of most prior years. It is hard to imagine the public markets seamlessly absorbing the wave of unicorn exits on the horizon, which begs the question: what share of the current private companies will succeed, and for those that fail, how will those losses impact the entire sector?

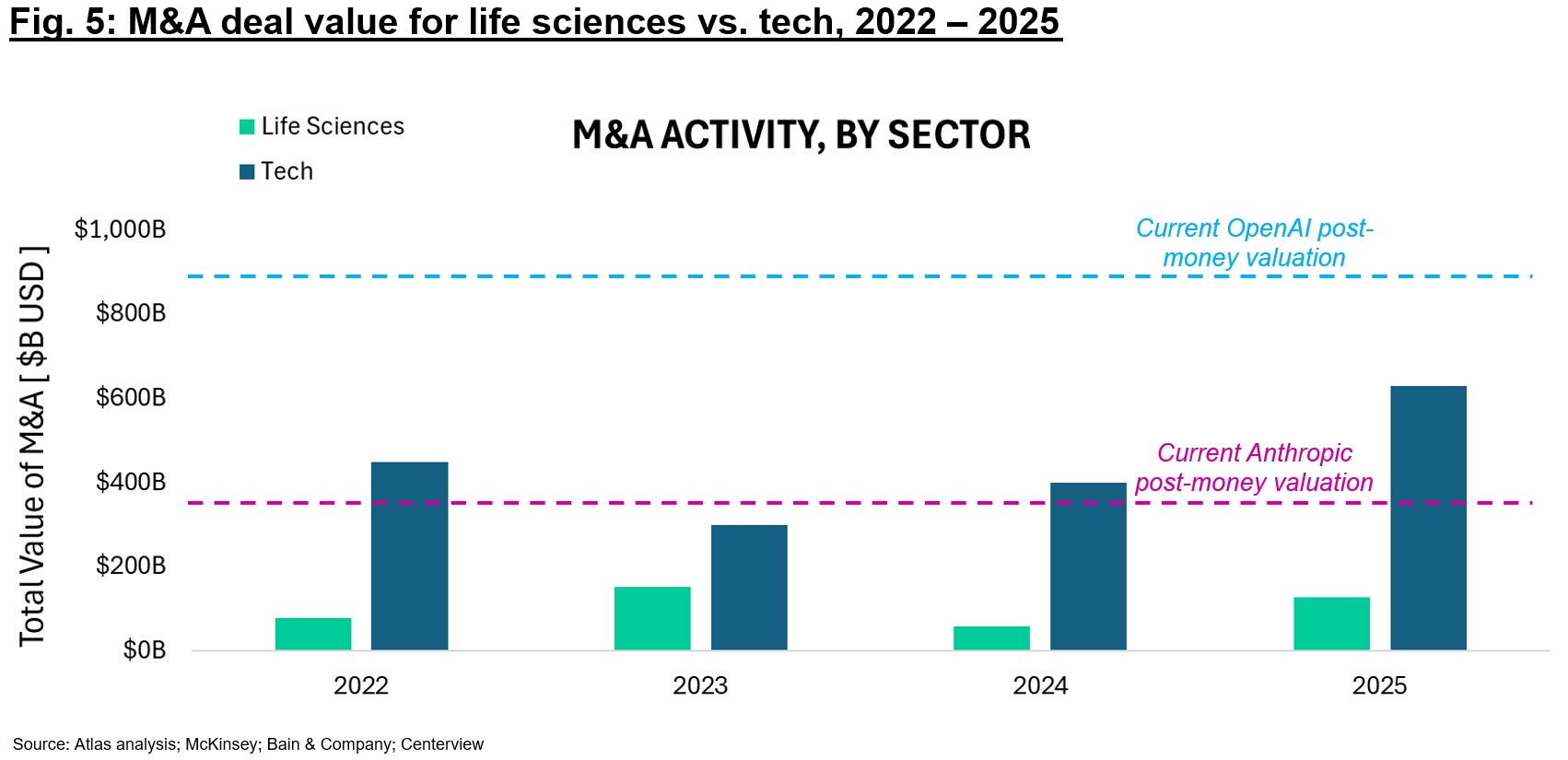

M&A is, of course, the other exit path – and biotech M&A in 2025 and early 2026 has been genuinely healthy. But here too, the numbers teach us that biotech M&A falls in the 10–20% range of total tech M&A. In Fig. 5, total M&A deal value for biotech (~$130B in 2025) is shown alongside tech (>$600B). A single acquisition of OpenAI or Anthropic at current private valuations could, in theory, exceed the combined M&A totals of biotech and tech combined – a striking illustration of the scale distortion that AI has introduced.

Reflections on the increasing capital intensity of our business

A few takeaways worth internalizing from this analysis:

- Life sciences, while a small piece of the overall venture pie, has delivered demonstrable value over time: it has produced highly valuable private companies, supported a healthy IPO ecosystem, and generated attractive M&A returns.

- Even so, the majority of venture financing flows to tech – and increasingly, to AI/ML specifically. The 2025 full-year figures (>65% AI/ML share) and Q1 2026 data (approaching 80%) suggest that we are still not at “peak AI.”

- Not everyone will win. The power law of VC returns is particularly unforgiving in capital-intensive sectors like AI/ML. Some firms will participate in the winners; many will be left holding stakes in capital-intensive companies that never achieve sustainable returns.

- Life sciences is fortunately less capital-intensive than compute-heavy AI, but there are lessons here for our industry. Life sciences investors are increasingly funding companies later into development, which does require more capital. Unlike in tech, biotech exits tend to be capped at roughly $5–10B in valuation (on the public markets or via M&A, with few notable exceptions). The math on power law returns looks different at that exit ceiling. Life sciences as a sector doesn’t support the same magnitude of concentrated winners that can offset a long tail of losses.

Ultimately, over-crowding into a hyped space has been shown time and again to compress venture returns. 2026 is an extraordinary training ground to test this hypothesis, as AI/ML is the most capital-intensive sector any investor has seen in their career. The cautionary tale is familiar even within our own small biotech ecosystem: we can all point to biotech companies that raised billions in financing only to fizzle out when their platform failed to produce differentiated programs. Or when a lead asset – despite “de-risked biology” – stumbled in multiple expensive Phase 3 studies. So, there are lessons learned from flooding into an over-hyped space and continuing to deploy capital even if the differentiation story doesn’t add up. Lucky for us in biotech, the cost of those mistakes in financing the “losers” are 1-2 orders of magnitude smaller than the associated costs for future AI/ML failures.

The story of capital formation versus destruction in AI will likely take this decade to fully resolve. I’m cautiously optimistic that the genuine productivity gains from AI will justify some (most?) of the capital invested. But the magnitude of capital at risk, and the pace at which that capital is being deployed, means the correction (when it comes) will be unlike anything prior technology cycles have produced. Our job in biotech, in the meantime, is to keep doing what we do: finance companies to serve unmet needs for real patients today, and hopefully with a reasonably defensible path to a meaningful exit for shareholders so that we can continue to invest in this space for decades to come. That may sound modest against the backdrop of >$800B AI valuations. But modest, in this environment, just might be a winning strategy.