DeFi lending protocol Edel disclosed a $403,000 exploit that hit the layer where tokenized stocks are trying to become DeFi collateral.

Edel said no depositor would bear losses, and the team would absorb the bad debt, restore affected balances one-to-one, and rebuild the protocol’s oracle architecture for a version two release.

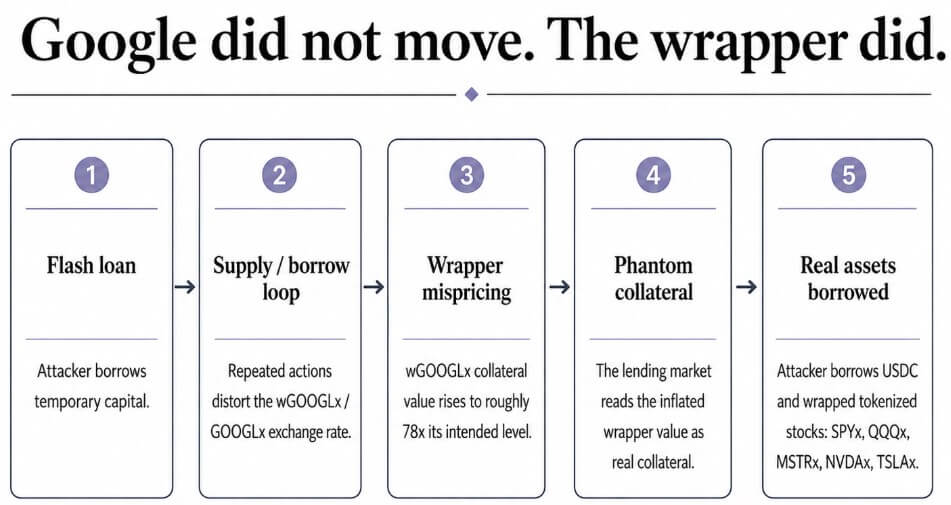

The attack manipulated the exchange rate between wGOOGLx, a wrapped version of Edel’s tokenized Google stock, and GOOGLx, the token it wraps. Edel said the manipulation pushed wGOOGLx’s collateral value to roughly 78 times its correct level.

SlowMist traced the root cause to Edel’s price source, which used latestAnswer() to return an ERC-4626-style vault’s convertToAssets() rate. That conversion rate can be manipulated when an attacker controls enough of the underlying flow, and Edel’s price feed reads it directly.

CertiK described the same flaw from the lending side: the attacker manipulated wGOOGLx’s collateral price, which tracked its GOOGLx balance, then borrowed against the inflated value.

GoPlus noted that the attacker used a flash loan to repeatedly supply and borrow, distorting the wGOOGLx/GOOGLx conversion rate. The inflated collateral then supported real borrowed assets, including 384,215 USDC and wrapped positions in SPYx, QQQx, MSTRx, NVDAx, and TSLAx.

Security firms published different estimates. Cyvers put the loss at roughly $353,000, GoPlus cited about $403,000 in losses and roughly $305,000 in attacker profit, and CertiK put the drained funds at roughly $204,000.

The gap appears to reflect different measurements, including bad debt, gross loss, and net attacker profit.

The disconnect probably comes from each firm measuring something different, such as bad debt, gross loss, or net profit.

The critical failure sat in the exchange rate between the wrapped token and its underlying counterpart, a relationship that Edel’s lending market priced as though it were stable. Alphabet’s share price did not drive the exploit.

The market in numbers

RWA.xyz puts tokenized stocks’ onchain value at $1.7 billion, up 2.17% over the past 30 days. Monthly transfer volume sits at $8.92 billion, and holders at over 396,000.

xStocks alone lists more than 100 stocks and ETFs across more than 50 integrated platforms, with over $25 billion in total transaction volume. It describes itself as fully backed and open to plugging into any DeFi protocol without permission.

Backed, the issuer behind xStocks, markets the tokens explicitly for DeFi use: lending tokenized Apple shares or borrowing against them without selling.

Kamino says it became the first major lending protocol to accept tokenized equities as collateral, allowing users to deposit tokens such as SPYx, QQQx, GOOGLx, AAPLx, NVDAx, TSLAx, MSTRx, and HOODx to borrow stablecoins or earn yield.

Robinhood launched stock and ETF tokens for EU customers in June 2025, then opened a public testnet for Robinhood Chain. The network is an Ethereum layer-2 built on Arbitrum, designed around tokenized real-world assets including equities, ETFs, and private assets.

The selling point across all of this is the same: tokenized stocks should move and connect like any other crypto asset. Edel is a reminder that once they move like crypto, they can also break like crypto.

| Market layer | What it enables | Examples from the article | Risk Edel exposed |

|---|---|---|---|

| Access | Users gain exposure to stocks and ETFs onchain. | Robinhood stock and ETF tokens for EU customers; xStocks’ 100+ stocks and ETFs. | Legal and issuer-level backing are necessary, but not sufficient. |

| Trading | Tokenized stocks move across venues, chains, and DeFi platforms. | xStocks across 50+ integrated platforms; $25B+ total transaction volume. | More integrations create more pricing and liquidity dependencies. |

| Collateral | Users borrow against tokenized equities. | Kamino accepting SPYx, QQQx, GOOGLx, AAPLx, NVDAx, TSLAx, MSTRx, HOODx. | Wrapped versions, vault exchange rates, and oracle paths can become attack surfaces. |

| Future derivatives | Tokenized equities become inputs for structured products and leverage. | Implied next phase as collateral markets mature. | A wrapper or oracle failure can spread beyond one lending market. |

The disconnect between backing and safety

A lending market prices several layers, such as the tokenized equity itself, the wrapped version built on top of it, and the exchange rate a vault uses to convert between the two.

It also prices the oracle path that reports a value, the lending market’s own borrowing limits, and whether that collateral can actually be sold during a period of stress. Edel’s exploit sat almost entirely in the wrapper and oracle layers.

Using a tokenized stock as collateral adds a second pricing problem on top of the equity itself. A protocol also has to price every on-chain representation built around that stock, including how a wrapper’s exchange rate behaves under stress. That exposure comes from the collateral integration built around a tokenized stock.

Flash loans, collateral manipulation, and ERC-4626 exchange-rate attacks have all shown up in DeFi exploits before. This exploit’s novelty lies in the asset class these techniques target, and it appears to be one of the first clear tokenized-stock-collateral exploits on record.

How this plays out

In the bull case, protocols spend the next year isolating wrapper risk. That means capping how much collateral in a lending market can come from wrapped tokenized stocks, separating issuer-level prices from wrapper exchange rates, and building oracle paths that a single flash loan cannot move.

Tokenized equities then become credible collateral for conservative borrowing against liquid names like Apple, Nvidia, Tesla, and Google. Edel ends up remembered as the early failure that forced better design before the category scaled.

In the bear case, listings outrun the risk work. More venues accept tokenized stocks as collateral before oracle design and wrapper isolation catch up.

The number of wrapped tokens, bridges, and vaults built around each ticker keeps multiplying faster than anyone can audit them.

Along that path, more exploits in the low hundreds of thousands of dollars continue to surface involving exchange-rate manipulation and thin liquidity. Tokenized stocks have become a security flashpoint over how DeFi protocols use them as collateral.

The first phase of tokenized stocks was access: letting eligible users hold tokenized exposure to names such as Apple or Google. The second phase was trading, which involved making that claim move across chains around the clock.

| Scenario | What has to happen | Market outcome | What Edel becomes in hindsight |

|---|---|---|---|

| Bull case: safer collateral markets | Protocols isolate wrapper risk, cap collateral exposure, separate issuer prices from wrapper exchange rates, and harden oracle paths. | Tokenized equities become credible collateral for conservative borrowing against liquid names like Apple, Nvidia, Tesla, Google, SPY, and QQQ. | An early failure that forced better design before the category scaled. |

| Base case: slower collateral adoption | Lending markets keep tokenized stocks in isolated pools with conservative loan-to-value ratios and tight caps. | Tokenized stocks grow mainly as trading assets, while borrowing use cases expand gradually. | A warning label that slows leverage but does not stop the market. |

| Bear case: listings outrun risk controls | More venues accept tokenized stocks and wrapped variants before oracle design and wrapper isolation improve. | More small-to-mid exploits appear around exchange-rate manipulation, thin liquidity, bridges, and vault accounting. | The first visible sign that tokenized-stock collateral became a security flashpoint. |

Edel arrived at the start of the third phase, collateral, where holding a tokenized stock also allows borrowing against it.

The first two phases of tokenized stocks rewarded whoever listed the most tickers or reached the most chains. The next one rewards whoever can price a wrapped stock correctly under stress, every time.